Health insurance is a vital part of ensuring that individuals and families are protected from high medical costs in case of illness or injury. However, for many people, obtaining long-term health insurance coverage may not always be practical or affordable. This is where short-term health insurance comes into play. Short-term health insurance is designed to offer temporary coverage during a gap in insurance or a transitional period. While this option can be useful in certain situations, it comes with both benefits and drawbacks. This article will explore the pros and cons of short-term health insurance, helping you make an informed decision about whether it is right for your healthcare needs.

What is Short-Term Health Insurance?

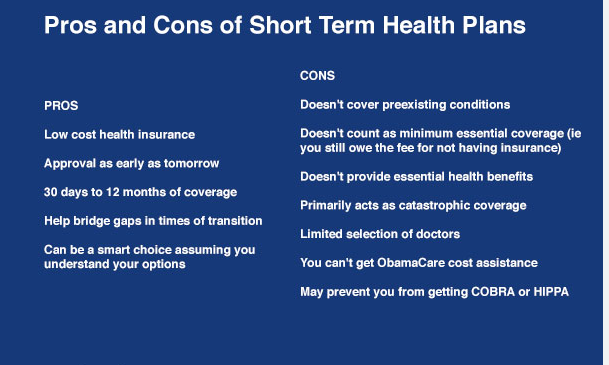

Short-term health insurance is a type of coverage designed to provide temporary health insurance for individuals who are in between other insurance plans. Typically, these plans last for a few months to a year and can be a more affordable option for those who have lost their previous health coverage or are waiting for other insurance plans to begin.

Short-term health insurance plans offer limited coverage compared to standard health insurance plans, such as those available through the Affordable Care Act (ACA). The plans may exclude coverage for pre-existing conditions, limit the types of care covered, and have high deductibles. Due to their temporary nature, short-term plans are intended to provide basic protection for people who need health insurance for a limited time.

Pros of Short-Term Health Insurance

While short-term health insurance may not be suitable for everyone, it can offer several benefits depending on individual circumstances. Below are some of the key advantages:

1. Lower Premiums

One of the biggest advantages of short-term health insurance is its affordability. Compared to traditional health insurance plans, short-term plans generally have much lower premiums. This makes them an appealing option for individuals who need health insurance but cannot afford the higher premiums of a full, long-term plan.

Short-term plans can be particularly useful for people who are between jobs, waiting for employer-sponsored insurance to kick in, or those who may have missed the open enrollment period for ACA plans. For individuals who don’t expect to need extensive medical care, a short-term plan can provide a more cost-effective solution to bridge the gap in coverage.

2. Flexibility in Coverage Duration

Short-term health insurance plans can be tailored to meet your specific needs, with coverage durations ranging from a few months to up to a year. This flexibility is ideal for individuals experiencing temporary gaps in coverage, such as a recent graduate, someone between jobs, or someone who missed the open enrollment period for an ACA plan. Depending on the state in which you live, some short-term plans may even allow for extensions beyond a year.

This temporary coverage gives individuals the freedom to choose when to seek more permanent, long-term insurance solutions. It allows people to have peace of mind while they transition from one coverage option to another.

3. No Enrollment Periods

Unlike ACA plans, which typically have specific open enrollment periods, short-term health insurance plans can be purchased at any time of the year. This makes short-term plans an attractive option for people who miss open enrollment for other health plans or experience an unexpected gap in coverage.

Since short-term plans don’t have enrollment periods, people can sign up whenever they need coverage, providing flexibility and quick access to health insurance. This can be particularly beneficial if someone unexpectedly loses their job, experiences a major life change, or needs coverage due to a personal emergency.

4. Customizable Plans

Short-term health insurance plans often offer customization options that allow individuals to choose coverage levels that fit their needs and budget. This may include choosing a higher deductible to lower premiums or selecting specific benefits like outpatient care or emergency services.

While these plans may not cover all healthcare needs, they can be designed to provide adequate coverage for individuals who do not expect to need extensive medical care during their temporary period of coverage.

Cons of Short-Term Health Insurance

While short-term health insurance can be a viable option for some individuals, it also has several disadvantages. Below are the main cons to consider before opting for short-term health insurance.

1. Limited Coverage

One of the main drawbacks of short-term health insurance is the limited scope of coverage it provides. These plans are not designed to cover all of the medical services that traditional health insurance plans cover. For instance, short-term health insurance often does not cover:

- Pre-existing conditions: Many short-term plans exclude coverage for pre-existing medical conditions, which means that if you have any ongoing health issues or prior medical conditions, they may not be covered under a short-term plan.

- Essential health benefits: Short-term plans typically do not cover all essential health benefits that are required under the Affordable Care Act. This can include preventive care, mental health services, prescription drugs, and maternity care.

- Chronic conditions and long-term care: If you have a chronic illness or need ongoing care, short-term health insurance may not provide the coverage you need. For people with long-term healthcare needs, a more comprehensive plan would be necessary.

The limited coverage of short-term plans can leave you vulnerable to unexpected medical expenses if you need care for conditions not covered by the plan.

2. High Out-of-Pocket Costs

While the premiums for short-term health insurance are lower than those of traditional plans, the out-of-pocket costs, such as deductibles, co-pays, and coinsurance, can be much higher. Short-term plans often come with high deductibles, which means that you may need to pay a significant amount of money out-of-pocket before the plan starts covering your healthcare expenses.

Additionally, these plans may have limited provider networks, which could lead to higher costs if you need to see specialists or visit out-of-network healthcare providers. If you require more extensive care, these high out-of-pocket costs can quickly add up.

3. Lack of Coverage for Preventive Care

Unlike ACA-compliant health insurance plans, short-term health insurance generally does not provide coverage for preventive care, such as routine check-ups, vaccinations, screenings, or wellness exams. Preventive care is a vital aspect of maintaining long-term health and preventing more severe health issues down the road. Without coverage for these services, individuals may be left to pay out-of-pocket for preventive treatments that could otherwise help them stay healthy and avoid costly medical problems in the future.

4. Exclusions and Limitations

Short-term health insurance plans often have significant exclusions and limitations. For example, if you are diagnosed with a serious illness or injury during your coverage period, your plan may only cover a small portion of the treatment costs. Additionally, some short-term plans may exclude coverage for certain medical services, such as maternity care, mental health services, or substance abuse treatment.

These exclusions can leave you vulnerable if you experience a major health event during your coverage period, as you may not be able to receive the care you need without incurring significant costs.

5. Short Duration of Coverage

While the flexibility in duration can be a benefit for some, the fact that short-term health insurance is designed for a limited period also means that it is not a long-term solution. Individuals who need consistent, long-term health coverage may find themselves needing to purchase another short-term plan or move to an ACA-compliant plan once the term expires. This can lead to continuous gaps in coverage, leaving individuals exposed to risks.

Conclusion

Short-term health insurance can be a useful option for people who need temporary coverage, such as those who are between jobs, waiting for other health plans to start, or experiencing a transitional period. Its affordability, flexibility, and lack of enrollment periods make it appealing in specific situations. However, it’s important to be aware of the limitations it offers in terms of coverage, pre-existing conditions, out-of-pocket costs, and essential health benefits.

Ultimately, short-term health insurance may be appropriate for healthy individuals who only need coverage for a short time and who do not anticipate needing extensive healthcare services. For those with more significant healthcare needs or who require long-term coverage, traditional health insurance plans may be a better choice. When considering short-term health insurance, it’s important to carefully evaluate your individual health needs, your financial situation, and the level of coverage you require before making a decision.