In today’s ever-changing world, health insurance is an essential safeguard for maintaining well-being and protecting against high medical costs. However, there are times when traditional health insurance plans, such as those offered through an employer or purchased on the Health Insurance Marketplace, may not be the right fit. For instance, if you’re between jobs, waiting for other coverage to kick in, or facing a temporary lapse in health insurance, short-term health insurance might be a viable option.

Short-term health insurance is designed to provide temporary coverage for individuals who need health insurance for a limited time. These plans are often more affordable than traditional plans, but they come with some significant limitations. Understanding both the pros and cons of short-term health insurance can help you make an informed decision about whether this type of coverage is right for you.

What is Short-Term Health Insurance?

Short-term health insurance, as the name suggests, is designed to provide coverage for a limited period, usually between 3 to 12 months. These plans were initially created to offer a stopgap for people who experience temporary gaps in health insurance, such as during a period of unemployment, a move between jobs, or a delay in the availability of other coverage.

Unlike traditional health insurance plans regulated by the Affordable Care Act (ACA), short-term plans are less comprehensive and are not required to cover essential health benefits (such as maternity care, mental health services, or prescription drugs). However, they can help cover certain medical expenses during the short period they are in effect.

How Does Short-Term Health Insurance Work?

Short-term health insurance typically works in much the same way as traditional insurance plans. You choose a plan based on the coverage options offered, pay a monthly premium, and are responsible for any co-pays, deductibles, and out-of-pocket expenses as outlined by the plan. However, short-term plans usually have more limited benefits, fewer provider networks, and lower premiums.

One of the most significant differences between short-term health insurance and ACA-compliant plans is that short-term policies do not need to meet the ACA’s requirements. As a result, they can provide more affordable premiums, but at the expense of comprehensive coverage.

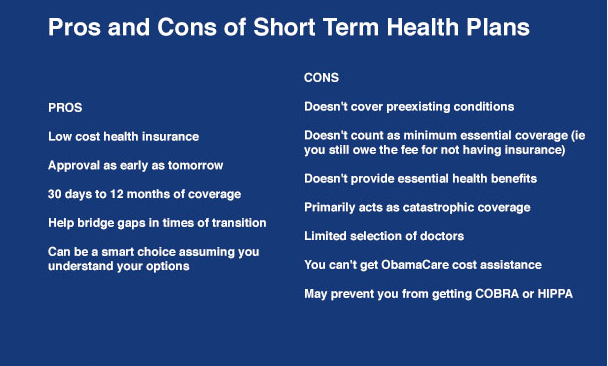

Pros of Short-Term Health Insurance

Short-term health insurance can offer several benefits depending on your personal circumstances. Below are some of the key advantages of opting for this type of plan.

1. Lower Premiums

One of the main attractions of short-term health insurance is its lower cost compared to ACA-compliant health insurance plans. Since short-term plans do not have to meet the ACA’s essential health benefits and consumer protection requirements, they can offer premiums that are significantly less expensive. For individuals who are healthy and in need of temporary coverage, these plans provide an affordable alternative to more expensive options.

2. Flexibility

Short-term health insurance is more flexible than traditional health insurance. You can choose coverage for as little as a few months, depending on your needs. If you’re waiting for other insurance coverage to start, or need a temporary solution, short-term insurance can bridge the gap.

Additionally, short-term plans often have shorter application processes, and approval times can be faster compared to traditional health insurance plans. This makes them a good option if you need coverage quickly.

3. Simplicity

Short-term plans tend to be straightforward and easy to understand. Unlike many comprehensive health insurance plans, which can have complicated terms and numerous exclusions, short-term insurance policies are typically simpler and easier to navigate. You’re able to review the basics of coverage, premiums, and the plan duration without wading through too much fine print.

4. Wide Range of Plans

Many insurance providers offer short-term health insurance policies, which means you can shop around and find a plan that works for your needs. Some short-term plans allow you to customize coverage based on what you’re looking for, whether it’s lower premiums or more extensive coverage for specific medical services.

5. No Long-Term Commitment

Because short-term health insurance is meant to cover only a short period, there is no long-term commitment. Once the coverage term ends, you can decide whether to extend your policy, seek other insurance options, or let the coverage expire.

Cons of Short-Term Health Insurance

While short-term health insurance can be a valuable option in certain situations, it also has several drawbacks that need to be carefully considered. Here are some of the key disadvantages:

1. Limited Coverage

One of the biggest downsides of short-term health insurance is that it typically offers limited coverage. Unlike ACA-compliant plans, short-term policies are not required to cover essential health benefits, such as:

- Maternity and newborn care

- Mental health and substance use disorder treatment

- Prescription drugs

- Preventive care and vaccinations

- Chronic disease management

This means that if you need comprehensive care, short-term health insurance may not be adequate for your needs. For individuals with ongoing health issues or specific medical requirements, a short-term plan may not provide the necessary coverage.

2. Exclusion of Pre-Existing Conditions

Short-term health insurance plans often exclude coverage for pre-existing conditions, meaning that any medical condition you had before enrolling in the plan will not be covered. If you are diagnosed with a health condition during the term of the short-term policy, treatment related to that condition will likely not be covered, leaving you with high out-of-pocket expenses. This can be a significant disadvantage for individuals who have pre-existing medical conditions.

3. Limited Duration of Coverage

Short-term health insurance is not designed to provide long-term coverage. In most cases, short-term plans last only for a few months, up to 12 months. While some states allow extensions, others may limit your ability to renew the coverage after the initial term expires. This limited duration means that individuals who need ongoing health insurance may have to frequently reapply for coverage or seek alternative plans when the term ends.

4. High Deductibles and Out-of-Pocket Costs

Although short-term plans tend to have lower premiums, they often come with higher deductibles, co-pays, and out-of-pocket expenses. In many cases, short-term health insurance plans require you to pay more out of pocket before the insurance coverage kicks in. For people who require regular healthcare or have significant medical needs, the higher out-of-pocket costs may make these plans financially unfeasible.

5. Not ACA-Compliant

Short-term health insurance plans do not comply with the Affordable Care Act (ACA) regulations. This means they do not meet the ACA’s essential health benefits or coverage requirements, and they do not guarantee coverage for certain services like preventive care, maternity care, or prescription medications. Additionally, short-term plans are not subject to the ACA’s protections against discrimination based on pre-existing conditions, which can leave individuals with health issues vulnerable.

6. Limited Network of Providers

Short-term health insurance plans often come with a restricted network of doctors, hospitals, and healthcare providers. This means that you may be limited in terms of where and how you can receive care. If you have a preferred doctor or specialist, they may not be part of the plan’s network, forcing you to either pay out-of-pocket or find a new provider.

Who Should Consider Short-Term Health Insurance?

Short-term health insurance may be suitable for individuals who find themselves in temporary gaps in coverage, such as:

- People between jobs or waiting for employer-sponsored coverage to begin

- Students or recent graduates transitioning to full-time employment

- Freelancers or self-employed individuals seeking temporary coverage

- Healthy individuals who need basic coverage for a short period and can handle higher out-of-pocket costs

However, it is important to note that short-term health insurance is not ideal for everyone. If you have pre-existing conditions, need comprehensive coverage, or anticipate needing long-term care, it is likely better to consider other options like an ACA-compliant health plan or Medicaid.

Conclusion

Short-term health insurance can be an attractive option for individuals seeking temporary coverage due to job transitions, waiting for other insurance to begin, or who are generally healthy and need basic health coverage. With lower premiums and flexibility, it may fit certain short-term needs. However, it comes with significant downsides, such as limited coverage, high deductibles, exclusion of pre-existing conditions, and a lack of comprehensive services.

Before choosing short-term health insurance, it is crucial to carefully consider your health needs, the duration of the coverage, and whether the plan provides adequate protection against potential medical costs. While it may be a good stopgap solution, it is not a long-term substitute for comprehensive health insurance. Always weigh the pros and cons to ensure it’s the right fit for your situation.